In the recent past, the economic challenges of Ghana have pushed the government to embark on sweeping policy actions that make policy analysts question the extent of analytical investments behind the big announcements, which often come with scant details. Understandably, these are desperate times.

Regardless, policy actions must not fail a basic systemic test of the overall implications they may have on the broader economy.

The role of gold in addressing the cedi depreciation and the attendant inflationary pressures has been exaggerated for the past six months. In July, there was a big announcement that the Bank of Ghana (BoG) would buy Gold as a reserve currency to promote the stability of the cedi.

Though this was touted as a novelty, the fact remains that the central bank has never been hindered from building gold reserves. The BoG has had arrangements with large-scale producers to purchase gold on an ongoing basis. It, therefore, did not require policy fanfare to purchase additional volumes of the tradable commodity, even if the goal was to pay the cedi equivalents for gold. Even countries that do not produce gold buy the commodity as a store of value.

A few months after the announcement to build gold reserves, the government announced a new policy to trade gold for refined petroleum products. This policy flip-flopping has generated ongoing discussions in the country, with many at sea on what exactly the government is doing.

Bright Simons has written on the subject and underscored the government’s difficulty in achieving its objectives of currency stability and cheaper petroleum products with gold.

I am particularly interested in the documentary effort because the government appears unfazed by the copious evidence that the country’s economic challenges are beyond the gold sector. Gold is indeed an important export commodity for Ghana, contributing about 35% of the country’s merchandise exports in 2021.

The irony, though, is that the gold sector contributes about 4% of the total GDP, an indication that the country instead has a limited export option. Unfortunately, this fundamental reality appears ignored in the hope that gold will do some more magic.

As a result, the space is inundated with political speeches seeking policy changes to target value from the export of the raw commodity. In contrast, the critical issues of value addition and local content development suffer in the hands of political businesses in the four-year electoral cycle. As a result, it is often about quick-win policies which fail to process risks and broader implications for the country.

In its attempt to rebuild reserves, either as a store of value or to trade for oil product government ended up providing an unsolicited hedge for gold producers, and a windfall never imagined in a turbulent gold market, a further testament that the risks were not adequately processed.

The average exchange rate between September, when the large-scale companies agreed to sell 125 thousand ounces of gold to BoG, and the first week in December was about 11.6 cedis to the dollar. Within that period, BoG bought about 100 thousand ounces of gold in cedis.

The sudden appreciation of the cedi in the middle of December to about GHS8 increased the values of the cedi paid to the companies by BoG by about 31%. In other words, the gold companies could convert the cedis paid to them to dollars at an average gain of 31%. The reverse is also true; BoG will get less cedis for the Gold it purchased over the period.

Making assumptions for the 100 thousand ounces, BoG used about 2 billion cedis, worth about $172.5 million, on the gold purchase programme.

Today the 2 billion is worth $250 million, about $77 million in trade losses in such a short period. Acknowledging that the gold prices have moved up a bit, the 100 thousand ounces is still worth about $180 million, leaving the trade losses significantly unmitigated.

The situation manifests that economic fundamentals cannot be replaced by coercive policy engineering, which tends to distort market confidence and enclave investments, such as the mining sector.

Beyond the trade bruises, which can be forgiven because it is a gamble which could have turned positive, we can interrogate the two underlying policy rationales for the gold purchase programme; as a reserve currency and “Gold 4 Oil”.

The original objective – gold reserve to underpin a stable cedi.

Many countries have continued to build gold reserves as a store of value post the gold standard era. The commodity has generally remained stable over the years after the collapse of the gold standard. Some countries also prefer gold for geopolitical reasons; they don’t like the dominant trade currency of the world, the dollar, and would hope it loses its relevance.

In the case of BoG, it sees gold reserves as a currency option to moderate the depreciation of the cedi. It is still unclear how the government conceptualised the connection between cedi stability and gold reserves, particularly when gold export was needed to bring in the dollars. However, two crucial facts are fundamental in judging the potency of the policy.

Firstly, the cedi does not depreciate because BoG doesn’t have gold reserves. It depreciates because BoG does not have enough reserves, dollars or gold, to manage the supply and demand imbalance of foreign currencies. Gold in the 21st century is directly convertible to the dollar; whichever the central bank held could be converted to meet the foreign exchange demand of the country. The external commitments of Ghana are primarily in hard currencies, mainly for the import of goods and services and debt service, making the dollar more potent to smoothen demand and supply imbalances.

The second important point is that gold has not been a better store of value than the dollar in recent history. In fact, BoG is better off with dollar reserves than gold. In the past two decades, the strength of the Dollar has been unmatched by any commodity or major trading currency.

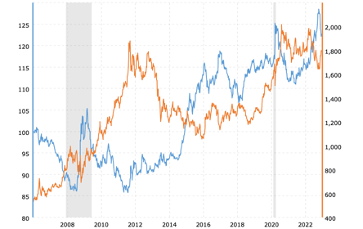

Trend of traded-weighted USD index and gold prices between 2006 and 2022

In 2011 when the gold price reached $1879.50, the highest of the first decade of the 21st Century, the trade-weighted US dollar index was 88.97. Today, the gold price is about $1800, against the dollar index of about 122. Across the timeline, the dollar has been more resilient than gold on a nominal basis.

Considering that the dollar is an interest-bearing currency, it is incredible how the central bank imagines it can stabilise the cedi by stockpiling a non-interest-bearing currency, gold, which is susceptible to significant price volatility. Last July, the gold price rallied to about $1800 in response to the Russia-Ukraine war. However, the intervention of the Federal Reserve through monetary policy tightening crushed the gold price by about 18%. That is not the kind of power BoG has. Moreover, by almost doubling the policy rate in a single year, inflation continues to smash records, again highlighting the limitations of monetary policy when fiscal policy is in dire straits.

GOLD 4 OIL

Before gold for reserve accumulation could settle, a new policy emerged in direct competition with the reserve objective; “Gold 4 Oil”. Since the announcement, many stakeholders have called for sunshine on what the government is imagining.

It immediately became clear that the policy was another unilateral dictate of the government without consultation. Checks with the entire gold value chain confirm the lack of consultation, leaving room for speculation and anxiety.

For example, the licensed gold buyers were unclear about how the new policy for the Precious Minerals Marketing Company (PMMC) to purchase small-scale gold would affect their trade. The president of the Chamber of Mines had the cause to ask for broader engagement on the policy at the Chamber’s Annual Awards night.

Beyond the challenge associated with a barter trade of two commodities effectively traded on the international market, with no scarcity expected, there are practical challenges that generate doubts about the feasibility of such a policy.

The Government agencies involved do not have a proven track record of pulling off this complicated trade. The Bulk Oil Storage and Transportation Company (BOST), Tema Oil Refinery (TOR) and PMMC are historically poor performers in oil and gold trading. Much of the energy sector debt problems are directly linked to the trading operations of state agencies. The PMMC has resigned from active trading to focus on assaying, having traded into a cash crunch.

It is, therefore, nervy for any serious analyst to imagine that these agencies would suddenly become efficient by controlling an “octopus” transaction in the nature of “Gold 4 Oil” to manage currency, gold, and oil price risks.

The most concerning issue is that government appears to have been telling the public a different story from what it is doing. On many occasions, government spokespersons have maintained that there was a government-to-government arrangement to trade gold for oil instead of the Dollar. However, it is now a fact that such an arrangement never existed.

In a recent presentation to stakeholders, the National Petroleum Authority (NPA) presented a transaction structure which reveals that oil products will be imported with the dollar, further clarifying that gold will not be exchanged for oil. According to the NPA, the oil supply will be backed by cash deposits and standby Letters of Credit (LC) in dollars. Why, then, is the government stretching the limits of integrity to signal markets to believe that the old fashion barter trade has reincarnated to distort market forces and dethrone the Dollar as the medium of exchange for petroleum products?

The structure presented as “Gold 4 Oil” only seeks to hand control of the gold and oil value chain to politicians. No other value can be deduced. It is obvious that if cheap oil comes to Ghana, other unknown factors will be responsible. Not gold. The government has still not been forthright about the cost of the structure to justify its competitiveness to the current private sector led approach. For the government to commence a potential $8 billion annual transaction (approximately $4 billion on gold and oil, respectively) with no credible information to the public on the parties involved in the external realm is terrible.

Interventions of this magnitude should not leave people in doubt. In the interest of good governance and assurance of the international community, which has shown significant interest in what Ghana is up to on the proposed “Gold 4 Oil” programme, all the necessary details of the transaction would be published, including the details of the external entities involved, both for gold and oil. The level of interest at the diplomatic level is far weightier than what is emerging as the transaction structure for a country in a debt bubble.

The government also needs to be cautious and guided by the challenging context of state agencies in the oil and gold business. When agencies make losses, the public pays. The energy sector is already inundated with debt because of similar trading abuses. There are no guarantees in the current structure that insulate the public from debt.

In fact, there is enough clarity to be less optimistic about what the turnout will be. When the government is not thinking about risks, a key function of effective trading, there is enough data in the energy sector to show that few politicians will make a quick buck at the expense of the public through debt. The public has paid over GHS30 billion in energy sector debt in the past six years.

BoG undoubtedly has an enormous responsibility within the current economic context, with inflation above 50 per cent. However, it risks losing credibility with the recent effort to embed itself so profoundly in commodities trading, particularly with historically inefficient agencies, it could end up with credibility exchange ahead of actual commodity exchange.

Petroleum Products constitute about 20% of total national imports. The country must also deal with 80% of the pressure on foreign currencies, including the import of food which can be produced in three months. At the same time, Ghana is close to importing 100 per cent of the chicken it consumes. Gold cannot solve these equally important problems of the country.

Government rather risks encouraging the smuggling of gold from the small-scale sector in the quest to monopolise the sector through its agencies. The country has been struggling to account for volumes of gold produced in the small-scale sector for years because of tax evasion and illegal gold traders who aggressively compete on price.

Making PMMC the sole gold buyer could be the worse that happened to the government’s efforts to raise tax revenue from the sector. Moreover, BoG’s exchange rate would be less attractive to gold producers, further risking the projected volumes needed for the “Gold 4 Oil” programme.

Merry Christmas!

****

Benjamin Boakye is the Executive Director of the Africa Centre for Energy Policy (ACEP).

Latest Stories

-

Alleged National Security operative remanded over GH₵1m recruitment scam

18 minutes -

Sametro Group of Companies donates to widows in Tarkwa Nsuaem Municipality to mark Christmas

38 minutes -

Morocco’s Family Code revision proposals unveiled in Rabat

2 hours -

Saglemi fire: No documents lost, redevelopment project unaffected – Oppong Nkrumah

2 hours -

WAEC uncertain about meeting Dec. 29 deadline for WASSCE results

3 hours -

‘She Leads Project’ calls for more female representation in politics to address women’s issues

3 hours -

DJ Promise crowned Best Radio DJ at Dangme Music Awards 2024

3 hours -

Re-collation: Court sets Dec. 27 to hear NDC’s suit against EC

3 hours -

Let’s remain positive, optimistic, and with calmness, rebrand our party – Afenyo-Markin

4 hours -

L’aîné HR celebrates 30 years of excellence in HR management in Ghana

4 hours -

Corporate Wellness: Elegant Homes emphasizes impact of Annual Health and Family Fun Day

5 hours -

BoG issues bancassurance directives to stakeholders in financial sector; warns of sanctions

5 hours -

African Paralympic Committee President sends festive greetings to fraternity

5 hours -

Ghana-Russia Centre holds its first corporate social responsibility event in Ghana

6 hours -

Mozambique’s opposition leader vows to install himself as president

6 hours