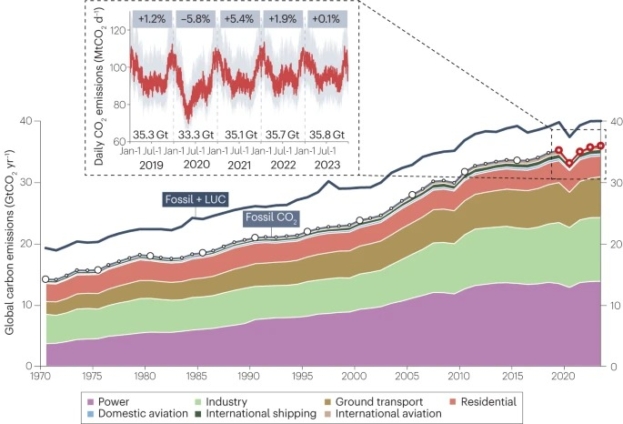

Global CO2 emissions in 2023 saw a marginal increase of only 0.1% compared to 2022, following higher increases of 5.4% in 2021 and 1.9% in 2022, reaching a total of 35.8 gigatonnes of CO2, According to data from the Carbon Monitor.

These emissions for 2023 accounted for 10–66.7% of the remaining carbon budget to restrict warming to 1.5°C, indicating that permissible emissions could be exhausted within 0.5–6 years with 67% likelihood. Despite the ongoing upward trend, there has been a deceleration in the rate of growth, suggesting that global emissions may have reached a plateau.

Data published on nature titled; Global carbon emissions in 2023 on 04 April 2024 indicates, total emissions stood at 35.3, 33.3, 35.1, and 35.7 in 2019–2022, resulting in year-on-year changes of –5.8% from 2019 to 2020, 5.4% from 2020 to 2021, 1.9% from 2021 to 2022, and 0.1% from 2022 to 2023. This slight 0.1% increase from 2022 to 2023 falls short of the 1.1 ± 1.0% increase projected by the Global Carbon Project (GCP).

As suggested by the International Energy Agency (IEA), the ongoing deceleration in growth rates could indicate a potential plateau or peak in global CO2 emissions in 2023.

A gigatonne (Gt) is a unit of mass equal to one billion metric tons. Therefore, 35.8 Gt CO2 represents a massive quantity of carbon dioxide emissions, often used in global carbon dioxide emissions, climate change, and environmental impacts discussions.

Sector by sector contribution

According to a published report in Nature, the sectoral contributions to global CO2 emissions remained largely consistent with previous years. The breakdown is as follows: the power sector accounted for 38.4%, industry for 29.0%, ground transportation for 18.6%, residential for 9.4%, international bunkers (including international aviation and shipping) for 3.5%, and domestic aviation for 1.0% of total global CO2 emissions.

The trend of decelerating growth in global emissions for 2023 is also noticeable at the sectoral level. For example, year-on-year changes in emissions from the power sector shifted from +0.9% in 2022 to -0.2% in 2023, while industry emissions transitioned from +1.6% to -0.8%. Similarly, residential emissions decreased from +0.9% to -5.5%, and international bunkers saw a decline from +18.1% to +8.9%. However, there were some exceptions: ground transportation witnessed an increase in growth from +2.5% in 2022 to +3.1% in 2023, and domestic aviation rebounded from -1.0% in 2022 to +14.0% in 2023. Nonetheless, both domestic and international aviation emissions remain below pre-pandemic levels, with 2023 emissions being -1.9% and -9.6% less than those in 2019, respectively.

Country by country level

At the country level, the combined emissions from the top five emitters have remained relatively consistent with previous years. In descending order, China, the United States, India, the European Union (excluding the UK), and Russia collectively contributed to 64% of global emissions, totaling 23.0 gigatonnes of CO2. However, interannual fluctuations are evident when comparing data from 2022 to 2023, making it challenging to predict long-term trends toward achieving zero emissions.

“For instance, emissions from China (the largest emitter) decreased by 1.9% to 11.0 Gt CO2 in 2022 but rebounded + 2.9% to 11.3 Gt CO2 in 2023. By contrast, other regions have maintained earlier increases. Emissions from India, for example, surged by 6.9% to 2.6 Gt CO2 in 2022 and by another 4.4% to 2.8 Gt CO2 in 2023; in doing so, India surpassed the EU to become the third-highest emitter. Russia exhibited a similar increase, whereby emissions increased by 1.0% to 1.5 Gt CO2 in 2022 and grew by 2.4% to 1.6 Gt CO2 in 2023,” the publication said.

As per the authors' findings, emissions started to decline in other regions as well. In the United States, emissions rose by 3.0% to 5.0 gigatonnes of CO2 in 2022 but decreased by 2.4% to 4.9 gigatonnes of CO2 in 2023. Similarly, the European Union's emissions experienced a slight increase of 0.3% to 2.8 gigatonnes of CO2 in 2022 but then decreased notably by 6.2% to 2.6 gigatonnes of CO2 in 2023.

Escalating Global CO2 Emissions Deplete Alarming Carbon Budgets

Global CO2 emissions are rapidly depleting the reported carbon budgets, which represent the amount of carbon that can be released while adhering to the temperature targets outlined in the Paris Agreement—1.5°C and 2°C above pre-industrial levels.

According to the Intergovernmental Panel on Climate Change (IPCC), with a 67% likelihood, the carbon budget for limiting warming to 1.5°C starting from 2020, and assuming no overshoot, was set at 400 gigatonnes (Gt) of CO2. Emissions from 2020 to 2023 depleted this budget by 38 Gt CO2 (9.4%), 39 Gt CO2 (9.9%), 40 Gt CO2 (10.0%), and an additional 40 Gt CO2 (10.0%) in 2023. This leaves only 243 Gt CO2 remaining, which could be exhausted within 6.1 years without significant emission reductions.

With an 83% likelihood, the post-2020 budget to avoid 1.5°C warming is even lower at 300 Gt CO2, with 2023 emissions depleting 13.3% of this budget. This leaves only 143 Gt CO2, potentially exhausted within 3.6 years. The carbon budgets for limiting warming to 2°C are larger, with a 67% likelihood budget of 1,150 Gt CO2, 3.5% of which was used in 2023. At an 83% likelihood, the 2°C budget is 900 Gt CO2, with 4.4% used in 2023. This leaves 993 Gt CO2 and 743 Gt CO2 remaining, respectively, which could be used within 24.8 and 18.6 years if emissions growth rates do not decline.

Other estimates of the remaining carbon budget suggest significantly lower permissible emissions. Under stricter constraints, only 250 gigatonnes (Gt) or 60 Gt of CO2 remain from January 2023 to achieve the 1.5°C target at 50% and 66% likelihood, respectively.

These estimates indicate a more urgent timeline. Focusing on the 66% scenario for comparison with the IPCC likelihoods, 2023 emissions utilized 66.7% of the budget, leaving only 20 Gt of CO2. At the current rate, the entire 1.5°C target could be depleted by mid-2024. In contrast, 1,200 Gt or 940 Gt of CO2 remains to limit warming to 2°C at 50% and 66% likelihood, respectively. For the 66% scenario, 2023 emissions accounted for 4.2% of the budget, leaving 900 Gt of CO2, which could be depleted within 22.6 years.

Latest Stories

-

Ahmed Suale murder: Suspect remanded in custody

13 minutes -

Ghana Rugby Football Union elections followed due process – NSA Boss

23 minutes -

#JoySports National Dialogue: You’re not a national federation if you only operate in Accra – Rex Danquah

30 minutes -

ISSER endorses the establishment of a value-for-money office to promote fiscal discipline

31 minutes -

GPL 2024/25: Legon Cities seek must-win against Vision FC to move out of drop zone

31 minutes -

Newly elected Rugby President Rafatu committed to growing sport in Ghana

48 minutes -

Let’s not compound our Free SHS problems with further freebies – Prof Peter Quartey

50 minutes -

Ghana faces fiscal tightrope amidst less ambitious 2025 growth targets – ISSER warns

57 minutes -

It’s important to learn from down moments – Otto Addo

59 minutes -

FDA orders immediate recall of Grand Chateaux Sangria Forte over safety concerns

1 hour -

Nigeria: President Tinubu declares state of emergency in Rivers State over pipeline vandalism

2 hours -

VRA/NEDCo staff oppose appointment of R.A. Abdul Jalil as Director of Public Affairs

2 hours -

Scrapping betting tax is a wrong move – ISSER to government

2 hours -

World Cup 2026Q: We need Chad, Madagascar games to bring back positivity – Otto Addo

3 hours -

Today’s Front pages: Wednesday, March 19,2025

3 hours