Finally, the elusive Chief Executive of the Ghana National Petroleum Corporation (GNPC) has found time in his packed diary to engage the public about the controversy surrounding the biggest single transaction in the GNPC’s history.

Alerted by friends, who know of my deep interest in the subject, I went online to watch the GNPC Boss’ interview on Ghana’s most popular local language radio station this morning myself.

Any thoughts I had about the purpose of the public engagement being about making up for the failure of the GNPC to conduct extensive consultations ahead of such a momentous decision, as indeed is required under the EITI framework to which Ghana subscribes, dissipated quickly as the interview progressed.

When asked to comment on the campaign of Ghanaian Civil Society Organisations (CSOs) against the GNPC’s recommendations to government to invest over a billion dollars in the two Aker-AGM blocks (Pecan and Nyankom), he dismissed every argument the CSOs have ever made out of hand, putting everything down to mischief or ignorance.

As far as he was concerned, nothing said so far by the CSOs has any merit, nor can the activists be said to be motivated by even the tiniest shred of genuine concern.

His way of dramatically illustrating his attitudes towards the CSO movement was to suggest that the analysis its members have so far been producing must likely be the result of “indigestion caused by fufu”.

Now, the CSO movement in Ghana has been accused of many things in the past, but excessive binging on fufu takes the prize for sheer imagination and vividity. It had to be fufu. What, with all the fears about cyanide in cassava and the well-known effects of starchy calories bloating the guts with mind-numbing gases, the image of CSO activists loading themselves full of the stuff before retiring to their rocking chairs to type nonsense is just the painting of alarm one expects the head honcho of a major parastatal to draw at this juncture.

Apart from the colourful fufu metaphors, however, there were few insights to filter from the interview on Peace FM and the subsequent ones on Joy FM, both major radio stations based in Accra.

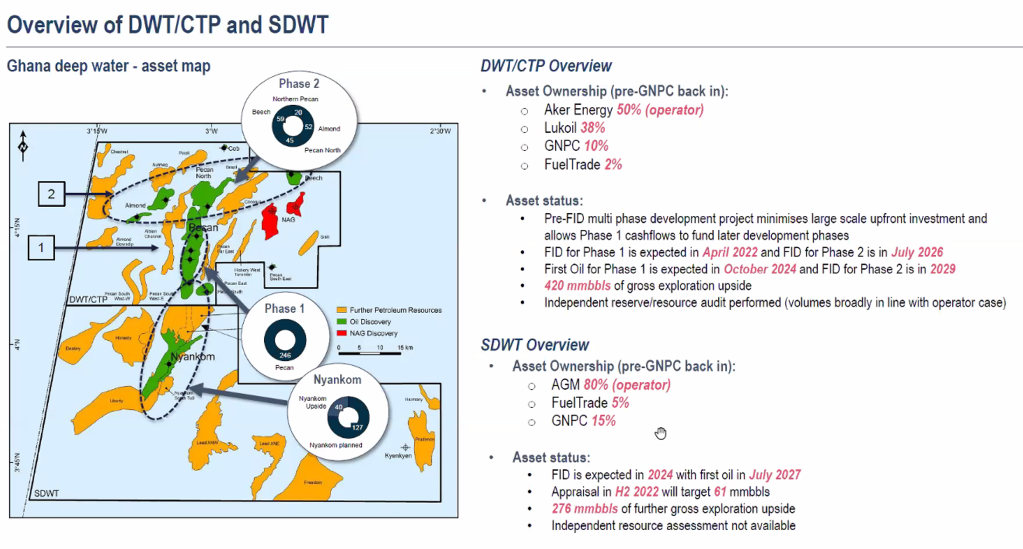

Having conceded that he finds Aker-AGM’s willingness to reduce their stakes to such low levels (10% for Nyankom and about 13% for Pecan) somewhat strange, the GNPC Boss’ only explanation for why Ghana conceded in the first place to hand over such massive rights, worth hundreds of millions of dollars, to Aker in June and December 2019 only to now buy them back at a premium was “desperation”.

Ghana, according to him, was so desperate to have Aker-AGM develop the blocks that it signed away precious concessions over only then to discover that Aker-AGM’s owners had set up three renewable energy companies, suggesting a disinterest in moving forward with the development and production of oil on the two oil blocks. But he still trusts them.

A much simpler explanation of course is that Aker-AGM knew where to find suckers: Ghana. They knew that it would be easier to offset all their risks upfront if they engineered this very state of affairs. Buy into two offshore blocks in Ghana for $135 million, convince the country’s pliant leaders to raise your stake for free, have laws changed to remove checks on you, and then return after you have failed to make the investments you promised to warrant all these candies to collect a cool billion dollars before handing back the country’s own assets back to them to hold the bulk of the risk for further development.

All the while retaining enough control of decision-making to ensure you are still in pole position to squeeze any margins from operations because your “joint operator” status remains intact. And should the poor, benighted, country still bumble its way into producing oil, well, your share is guaranteed. Only upside, never downside!

Ghana is not a country where leaders get asked hard questions. It was cringeworthy listening to the GNPC Boss make one implausible claim after another without a single rebuttal. In accounting for the shocking about face in 2019 which saw hundreds of millions of dollars of rights handed over to Aker only for the country to buy them back in just a year and half, he returned to the hapless theme of “energy transition”.

In his world, no one knew of the energy transition in December 2019 when Parliament of Ghana was signing bonanza after bonanza off to Aker, based on the GNPC’s advice.

His esteemed team, one must assume, missed the commitments made by the energy majors in 2017. Though excessive fufu eating is unlikely to be the cause, something else must have plugged their ears and covered their eyes.

They never heard about the Oil & Gas Climate Initiative and the strong endorsement of Net Zero (carbon emissions neutral) oil operations by the oil majors in 2016 either. Begs the question: can Ghanaians trust a GNPC leadership so cut off from the strategic trends in the industry they operate?

Anytime a GNPC executive talks about the energy transition as being a sudden development warranting kneejerk remedies to long-term strategic problems they have created, they worsen fears about their current actions.

Nor was the head honcho of the GNPC averse to abject disinformation. His claim is that before Hess sold the Pecan block, the largest of the two blocks in controversy, to Aker for $100 million, they had spent a whopping $1.2 billion developing it.

Very dangerous stuff. If Hess had spent that much and exited at $100 million, they would have recorded massive write-offs. But we know from their annual report covering 2018 (pages 10, 21, and 32 especially), the year they sold out to Aker, that they wrote off less than $300 million.

GNPC’s continued efforts to inflate these “inherited costs” have massive implications down the line since our petroleum tax laws allow investors to recover some of the money they spend finding oil from the State through tax credits.

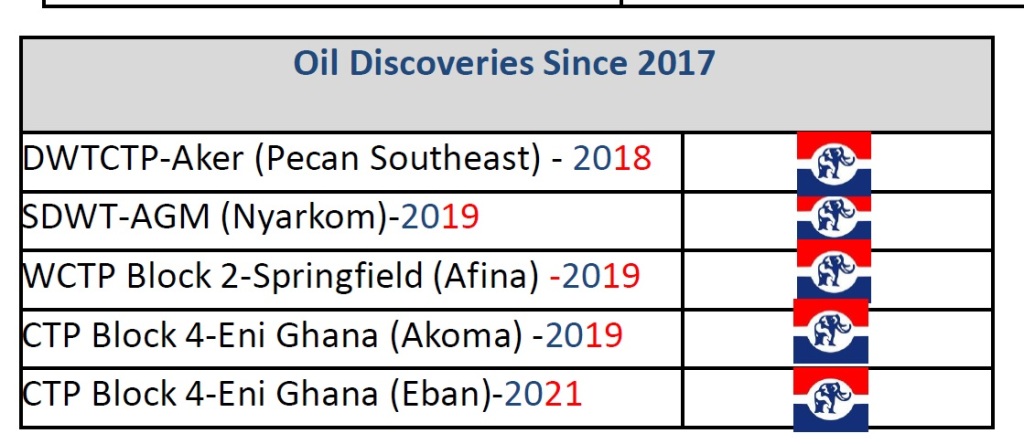

In a similar vein, he brazenly claimed that Aker’s discoveries since they bought Pecan exceeds 100 million in additional net oil resources. Yet in a presentation he made to the Cabinet and the Economic Management Team, it is clear that the only discovery made on Pecan by Aker is Pecan South East.

The true picture, badly distorted in the interviews with Peace and Joy radio stations, is that Aker itself at the end of the entire appraisal campaign, which included all the 3 wells they drilled following their 2018 purchase of the Pecan block from Hess, which you might remember had already drilled seven successful wells before selling out to Aker, concluded that the total estimated new oil resources discovered were between 5 and 15 million barrels of oil.

To have a situation where the Head of a National Oil Company is inflating the resources added by a foreign company in order to justify paying them more than they deserve is beyond frightening.

For those not too familiar with the subject, it bears emphasising the point: when Aker bought Pecan from Hess in 2018, the latter company had already drilled seven wells and made a firm estimate of discovered oil volumes of 340 million barrels. It had also found evidence suggesting additional volumes to the tune of 110 and 210 million barrels of oil could be recovered from under the ocean floor. Most of this work was done by 2013. Aker comes into the picture in 2018, drills three wells and conclude that an additional amount of between 5 and 15 million barrels of oil could be extracted. The CSOs consequently make the argument that since buying into the block for $100 million, Aker has not changed the commercial picture significantly for GNPC to want to pay the billion dollar figures they have been bandying around. To discredit the CSOs, the Chief Executive of GNPC concocts a mysterious figure of 100 million barrels as the additional discoveries made in Pecan.

Following the same pattern, he proceeds to accuse CSOs of lying about the potential of competing assets in Ghana’s oil basin to undermine the arguments his organisation has made for the commercial uniqueness of the Aker-AGM blocks, for which reason Ghana must pay so much just for the right to take the larger share of risks in developing them.

What did the CSOs say? We argued that if GNPC did not have an underhand interest in the Aker-AGM deals, they would have benchmarked the attractiveness of the Aker-AGM blocks with other “stranded” assets (commercial and sub-commercial discoveries that have not been developed by their lease owners in Ghanaian waters).

We deliberately highlighted discoveries that the IHS Markit Resource Ranking databases suggest have more contingent resources (loose estimates of oil volumes) or reserves (firm estimates of oil volumes) than Nyankom, the second and smaller of the two Aker-AGM blocks that GNPC believes is worth over $800 million and is aiming to acquire for nearly $400 million. These include the likes of Kosmos’ Wawa and Akasa and the abandoned Dzata block.

We also pointed out a particular block, which we would call the “Erin Block”, after its now bankrupt former operator, where far more work has been done than Nyankom. So far, only two wells have been drilled on Nyankom, and one was a hopeless disappointment. The Erin block on the other hand has seen as much as 14 wells drilled since the 70s, with considerable test production. The GNPC head honcho takes issue with our suggestion that Erin has contingent resources of 500 million barrels of oil equivalent compared with Nyankom’s highly speculative 127 million barrels (according to data provided by GNPC and Aker to Lambert). “Highly speculative” because Aker has not been able to come up with an official volume analysis estimate to its shareholders since promising to do so in its 2019 letter to shareholders, and also because only one successful (slim-bore) exploratory well has been drilled in Nyankom, and that unappraised. The GNPC Boss insists that Erin has sub-commercial volumes in the region of 50 million barrels.

In essence, the Head of the country’s National Oil Company (NOC) is bastardising blocks in the country’s oil basin that are still on the market looking for investors. Even after an independent reserves auditor has established contingent resources of 500 million barrels, the NOC Chief, because of his parochial interest in another deal, is broadcasting to the whole world not to come for this stranded block. Unbelievable! Of all the dangerous things the GNPC Boss said in his hurriedly arranged interviews, designed to ensure that no serious questions would be asked, this one takes the biscuit!

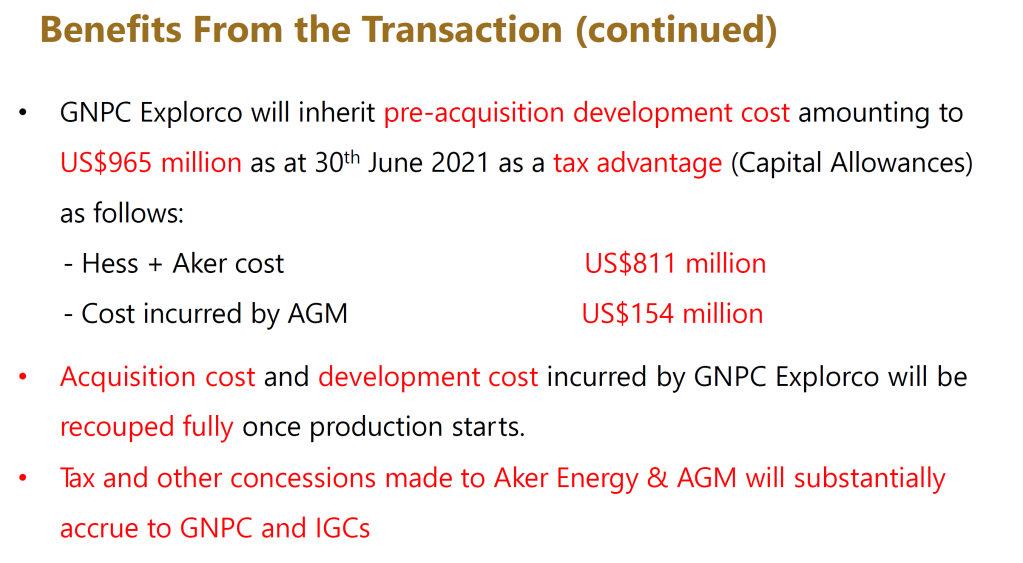

As if all the preceding was not enough, he started serving the Ghanaian public different numbers from what they had communicated to the Economic Management Team, Cabinet and television.

On page/slide 49 of the now legendary presentation by the GNPC to Government, the numbers indicated as capital costs on Pecan and Nyankom by Aker-AGM totalled $965 million (see below). This number is of course in conflict with the $1.2 billion that the GNPC boss now claims Hess spent on Pecan (which we dispute above), plus as yet unconfirmed amounts spent by the previous holders of the Nyankom block. The over $1 billion in costs are to be offset in the future by GNPC, Aker and a string of as yet unnamed “indigenous oil companies” against tax liabilities, without regard to depreciation and tax statutes of limitations, meaning simply that taxes owed the state will not be paid.

Yet, during his interview, the numbers metamorphosed to $1.2 billion spent by Hess and $712 million spent by Aker and a host of finance charges he claims the foreign oil companies are right to saddle Ghana with.

As I have explained clearly and simply above, the foreign oil companies are owned by entities registered in their home countries. They file returns and taxes in those places. Their costs are duly recorded in compliance books. Hess disclosed spending of $280 million. Aker has disclosed spending in the region of $200 million. Adding a dime here and a nickel there, and making provisions for spending by passive partners, take us to roughly $600 million as eligible investments in the field so far.

Their willingness to inflate the amounts that these companies have spent in Ghana so far merely goes to reinforce our suspicions of GNPC’s motives. Especially also when such number gaming is used to justify crazy valuations and lay the grounds for future tax heists.

One of those suspicions relate to the role of as yet unnamed “indigenous oil companies” that are supposed to be introduced into the joint venture entity GNPC is proposing to integrate their operations with Aker’s after the acquisitions.

There have been serious controversies over the involvement of Fueltrade in Aker-AGM matters because the son of the GNPC head honcho is the CFO there. So when Lambert in its valuation presentations (see below) suggests a quiet sale of Quad’s stake in Nyankom (SWDT) to Fueltrade, one’s unease about the real dynamics at play here grows. Especially when CSOs had previously accused Quad of being a mere placeholder for others during the early campaign against the Government’s plans to downgrade Ghana’s stake in the Aker-AGM blocks (the same stakes that are now being repurchased at a premium).

No matter how anyone dices or minces it, the position of the CSOs remains robust so far: Aker-AGM has not done enough to de-risk the two oil blocks since paying $135 million for both. To the extent that the commercial picture has remained stagnant since they last bought them, and the external environment for fossil fuels worsened, leading to likely higher breakeven costs of production (decarbonisation pressures, equipment scarcity and lower investments in extraction technologies) and lower prices (major analysts now projecting a long-term oil price of $50) in the future, GNPC should not pay more than $400 million (or $2 per pro rata proven reserve barrel) to acquire the majority rights to participate in this highly risky venture.

A cue can be taken from Total’s acquisition of Tullow’s 33.3% stake in the much more prolific Lake Albert basin in Uganda for $575 million, where the French major updated the market with pride about paying less than $2 per barrel.

With only 340 million estimated reserves (repeat: Nyankom has not been properly audited, much less appraised) and the production horizon much farther into the future, GNPC’s willingness to pay roughly $7 per barrel is completely ridiculous.

If such counsel requires eating bowlfuls of fufu to arrive at, can we recommend that the GNPC Boss tries same, but with prekese-infused soup?

Latest Stories

-

Let’s be careful CJ’s removal process doesn’t become a political tool – Dr Osae Kwapong

5 minutes -

We have not received complaints about politicians being involved in galamsey – EPA boss

8 minutes -

GhIE holds closing banquet & Engineering Excellence Awards

12 minutes -

Government enacts landmark Public Financial Management Act to enhance fiscal discipline

18 minutes -

Ghana Italian Women and Men Association donates over 2,000 furniture to schools

19 minutes -

Expanding Ghana’s healthcare market: the rise of medical tourism

40 minutes -

Zimbabwe police arrest dozens in wake of protests

60 minutes -

Ethiopia unveils 100 electric buses in Addis Ababa

1 hour -

Ghana’s Resilience: Preparing for the rains ahead

2 hours -

Val Kilmer, ‘Top Gun’ and Batman star with an intense approach, dies at 65

2 hours -

Ghana’s Selassie Atadika named in 2025 TIME Earth Awards

3 hours -

Maiden Ofie Market records massive patronage as traders, farmers laud Sammi Awuku

3 hours -

World Autism Day: Let’s continue to promote acceptance

4 hours -

Corporate tax affecting rural financial institutions

4 hours -

Columbia University protester Khalil’s case to remain in New Jersey

4 hours