Audio By Carbonatix

1. The genesis of the affair was in 2018 when the Ghanaian tax authorities (GRA) decided to audit Tullow’s tax filings from 2012 to 2016. In December of that year, GRA concluded that Tullow had cheated Ghana of tax due to the tune of ~$140 million for 2013 and 2014. Tullow promptly filed a protest with the Commissioner General.

2. Tullow’s protest seemed to have angered GRA even the more. In December 2019, GRA came back and said that Tullow actually owe Ghana ~$331 million in back taxes covering 2012 to 2016. Tullow continued to insist on its innocence in the matter.

3. Eventually, in September 2021, GRA shaved off some coins, reducing Tullow’s liability to $320 million. Finally exasperated, Tullow demanded arbitration under its Petroleum Agreements with Ghana at the International Court of Arbitration (ICA) of the International Chamber of Commerce (ICC) in London, UK.

4. GRA’s computation of Tullow’s tax arrears was based on a notion that Tullow’s sending of profits it had made in Ghana from producing and selling its share of oil to its head office in the UK ought to have attracted a withholding tax. To the extent that Tullow didn’t withhold and pay this tax to Ghana, Tullow had cheated the country.

5. Tullow’s counterargument is that it would be double-taxed if it followed GRA’s prescriptions since its profits had already been taxed, and at any rate, its agreements with Ghana do not allow any forms of tax other than what was specified in the agreement to be applied. Tullow’s agreements with Ghana had been signed on the back of petroleum laws made in the 1980s. To attract certain classes of investors into their country, governments normally promise them that the terms of their investment will remain “stable” throughout. Taxation, being one of the most critical considerations for any foreign investor, tend to be one of the principal elements captured by so-called “stabilisation” provisions in such agreements. (Of course, by the same reckoning, Tullow continued to pay corporate income tax at a rate of 35%, which is what prevailed at the time of the agreement, instead of the lower 25% today. )

6. Tullow thus argued that it was only to be taxed based on the terms of the Agreements it has signed with Ghana and not on the basis of the country’s general tax laws. What is more, it does not operate through a subsidiary in Ghana. Instead, it has a local branch of its entity incorporated in Jersey, a tiny European country nestled between England and France. The head-office of this entity was initially in the Netherlands but has since been moved to the UK. In Tullow’s view, the branch and head-office together constituted a single entity. Thus, moving profits from the branch in Ghana to the head-office in the UK is a mere accounting step like passing money from department to department in the same corporation. Such transfers shouldn’t and can’t be taxed.

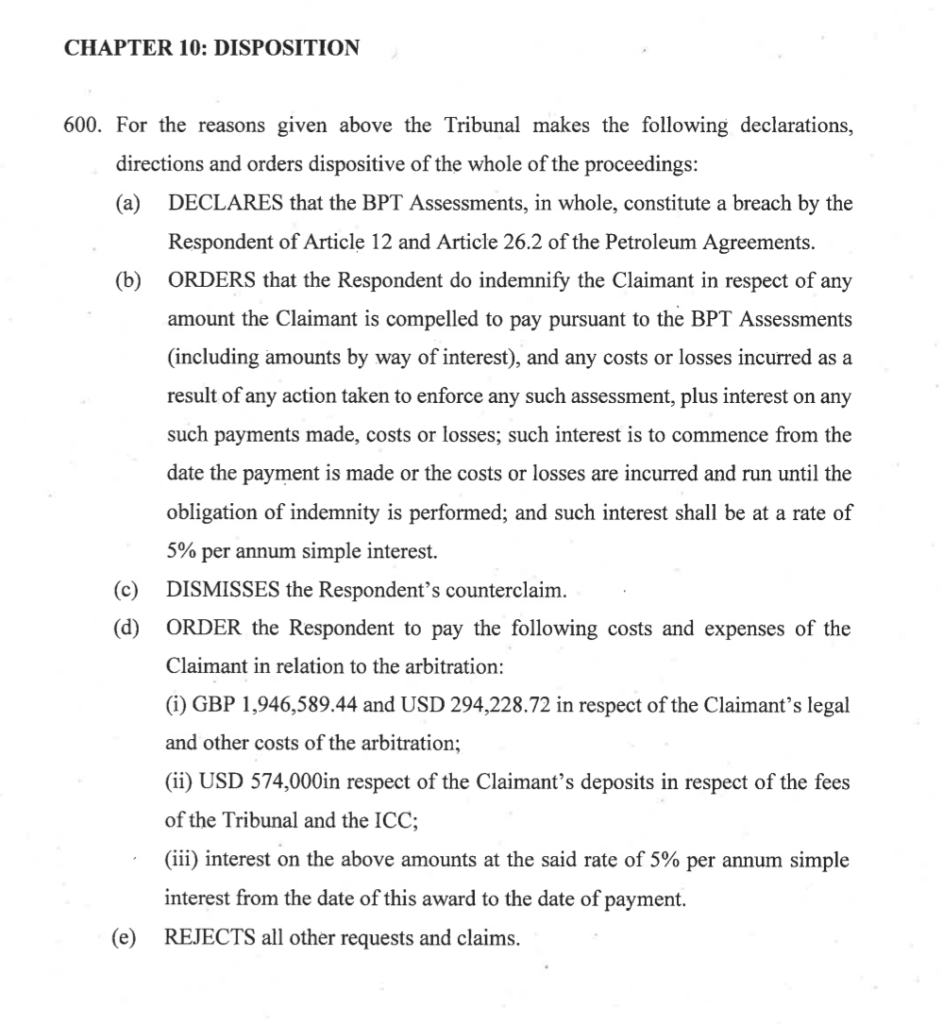

7. After more than three years of vigorous debate, the arbitration panel ruled late last month that having signed those agreements with Tullow in 2004 and 2006 stating clearly that the Anglo-Irish company would be taxed based on their express provisions, the government of Ghana was simply wrong in trying to squeeze more money out of Tullow than warranted.

8. There is an aspect of GRA’s position that reasonable people can feel sympathy towards. GRA argues that had Tullow incorporated a subsidiary in Ghana, there would have been no debate about taxing its repatriated profits to overseas affiliates or parents. Hence, it is unfair to other mining and petroleum companies who use the parent-subsidiary structure if those who use the headoffice-branch structure can avoid paying taxes on what the GRA feels amount to ordinary dividends. Furthermore, even the arbitration tribunal concedes that the Income Tax Act of 2015 seeks to delineate the legal difference between branches and their head-office affiliates even if the same tribunal also contends that the 2015 Act did not apply to most of the profit repatriation transactions in issue.

9. The issue here is that the Agreements signed, at a time when Ghana was desperate for investment into its petroleum sector, made it very clear that all taxes and charges have to be explicitly stated for them to apply. No Branch Profits Taxes or other Withholding Taxes were mentioned. To get around this, the government’s lawyers tried a half-baked argument that the profits sent to the UK by Tullow were not covered by the stability and limited-taxation clauses in the Agreements because they should be classed as “investment income” rather than income derived from petroleum operations, or “business income”.

10. The government was hoping to persuade the arbitration panel that sending money overseas to a head-office or affiliate, or whatever, isn’t, strictly speaking, “petroleum operations”. Therefore, even though the Agreements said that any income derived from petroleum operations can only be taxed in the ways specified in the Agreements, Tullow’s profit repatriation isn’t covered by the protection since it is an “activity” separate from actual petroleum operations. Sharp readers would have guessed already that this was too twisted an argument to find favour. The arbitrators simply responded that since the money ultimately mostly came from petroleum operations, it was covered.

11. It is interesting that the Ghanaian Appeals Court in 2023 overturned a decision by GRA, endorsed by the High Court, that sought to use the distinction between “investment income” and “business income” to deny Perseus Mining the right to deduct certain expenses from its income for tax purposes. Here too, the Appeals Court ruled that the activities (financial derivatives) giving rise to those expenses were intimately connected with Perseus’ operations despite GRA’s protestations to the contrary.

12. Had the proceedings stayed strictly within the limits of argumentation as described above, I would have been inclined to cut the Attorney General some slack in this case. But certain things happened that showed that very poor advice was given to GRA and that under no circumstances should things have been allowed to degenerate to the point where Tullow had no choice but to proceed to arbitration.

13. It became clear, and the government of Ghana was forced to concede, during the proceedings that the GRA had applied the formula in the International Revenue Regulations of 2001 wrongly in calculating the back taxes for Tullow. The bizarre mistake led to a variance of a whopping $137 million, denting the credibility of the government’s submissions. Clearly, had the Attorney General properly reviewed GRA’s case before crossing swords with Tullow in London, such an embarrassment would have been avoided. Attentive readers might recall that similar technical lapses by the GNPC lie at the root of another embarrassing arbitration episode involving Ghana’s Attorney General, the Eni-Vitol one.

14. Then less than two months to the conclusion of the case, the Attorney General attempted to have the President of the arbitration panel removed from the case on very frivolous grounds. Obviously, he lost. Not surprising then that even though the panel had up to February 2025 to issue its ruling, it did so last month. I won’t be surprised if they had had enough of the Attorney General’s antics and convoluted reasoning.

15. Going forward, the government of Ghana should ensure that disputes are mediated rigorously before matters proceed to court or arbitration. The millions of dollars imposed as costs on Ghana in this Tullow matter, plus what has been spent on expensive international lawyers, could have been put to better use if negotiations had been thorough right from the beginning.

At least, the government would have become aware of GRA’s shaky math and taken another look at its other determinations. The incoming government inherits another arbitration dispute with Tullow, another multimillion dollar assessment. Let us hope its assigns would draw all the right lessons and be more tactful. They may even find some inspiration from a case, a decade ago, in which Uganda meticulously pursued $400 million in back-taxes from another Jersey-based petroleum firm and eventually forced its buyer, the same Tullow, to pay up without fudging the math or confusing contractual and statutory terms.

Latest Stories

-

Ghana’s global image boosted by our world-acclaimed reset agenda – Mahama

4 minutes -

Full text: Mahama’s New Year message to the nation

5 minutes -

The foundation is laid; now we accelerate and expand in 2026 – Mahama

24 minutes -

There is no NPP, CPP nor NDC Ghana, only one Ghana – Mahama

26 minutes -

Eduwatch praises education financing gains but warns delays, teacher gaps could derail reforms

40 minutes -

Kusaal Wikimedians take local language online in 14-day digital campaign

1 hour -

Stop interfering in each other’s roles – Bole-Bamboi MP appeals to traditional rulers for peace

2 hours -

Playback: President Mahama addressed the nation in New Year message

2 hours -

Industrial and Commercial Workers’ Union call for strong work ethics, economic participation in 2026 new year message

4 hours -

Crossover Joy: Churches in Ghana welcome 2026 with fire and faith

4 hours -

Traffic chaos on Accra–Kumasi Highway leaves hundreds stranded as diversions gridlock

4 hours -

Luv FM Family Party in the Park: Hundreds of families flock to Luv FM family party as more join the queue in excitement

4 hours -

Failure to resolve galamsey menace could send gov’t to opposition – Dr Asah-Asante warns

4 hours -

Leadership Lunch & Learn December edition empowers women leaders with practical insights

4 hours -

12 of the best TV shows to watch this January

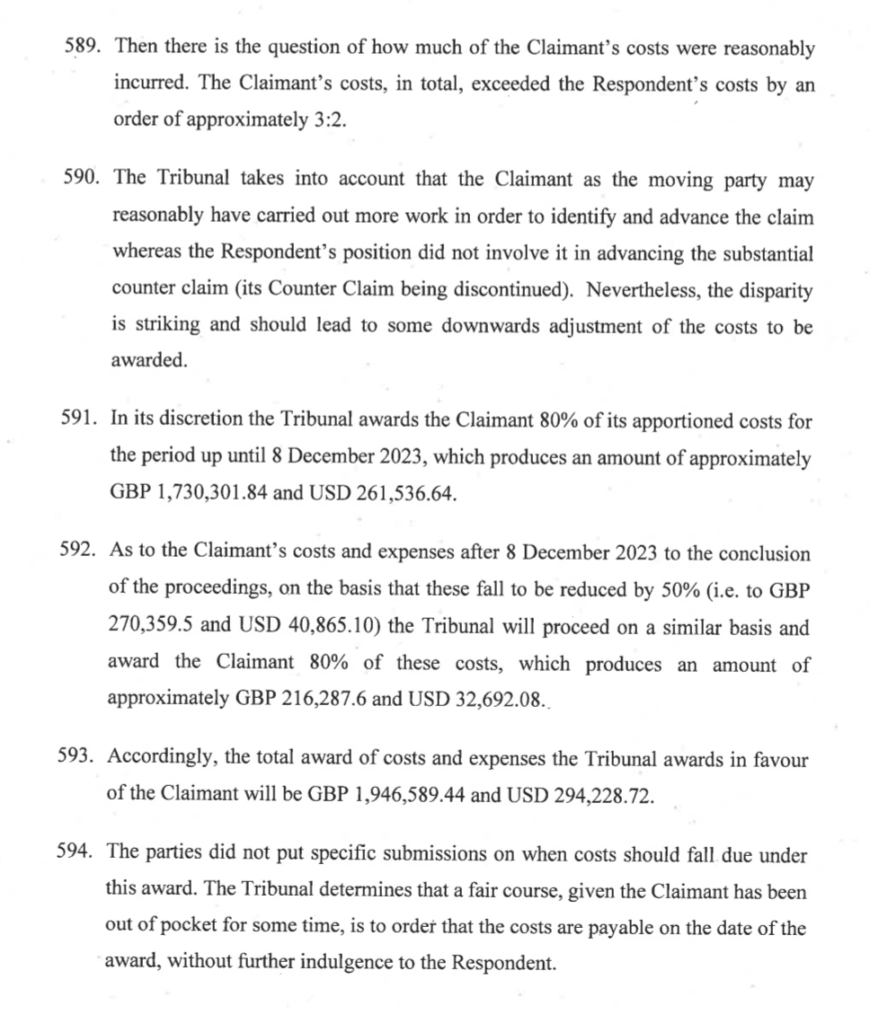

5 hours