PART 1: Nana Addo gets more in 3 years than Mills/Mahama in 6 years

Introduction

The Government keeps repeating that its predecessor left a weak economy at end-2016. In trumpeting this view, it deliberately ignores the legacy of opportunities created, despite major challenges.

Rather, its distortion of 2016 data and poor performance from 2017-to-date is exposing a worse legacy at end-2020. It strenuously but fails to blame huge pre-COVID-19 fiscal gaps from distorted data since 2017 on the pandemic.

The revisions and qualification of data by this writer, Parliamentary Minority and now by the IMF, World Bank, and other reputable institutions is ongoing. Further, recent downgrades by all the major ratings agencies expose frightening fiscal outcomes since 2017—long before the impact of COVID-19 in 2020.

Ghana just posted its first negative growth in a quarter in nearly 40 years and, with the current pandemic and past crisis as background, there is increasing awareness of what it took for HE Mahama to keep the nation from the recessions that hit African and non-African countries from 2014 to 2016.

This article deflates the false claims of poor legacy at January 2017 with facts and figures while restating that the immediate-past government put the present one in a position to manage the economy better than the negative and worrisome indicators and trends that are worse than a challenging end-2016—and all the current deterioration is not on account of COVID-19.

Parts 1 and 2 begin with the endownment of oil production and revenues while Part 3 makes the case that HEs Mills and Mahama did not more with one (1) oil field than HE Nana Addo is doing with three (3) fields. The remaining parts repeat the revisions of data in detail, as a portrayal of a frightening FY2021 ahead of the nation.

- Benefits of Petroleum Revenues

The obvious Mahama legacy is the two (TEN and Sankofa) additional petroleum fields that started to generate revenues at the start of HE Nana Addo’s administration in 2017.

It has become the beneficiary of over half of the total oil revenues in three (3) years, more than the combined HE Mills/Mahama inflows for six (6) years. These Mahama investment outcomes, while navigating several crises, resulted in a 2017 turnaround that has become sour.

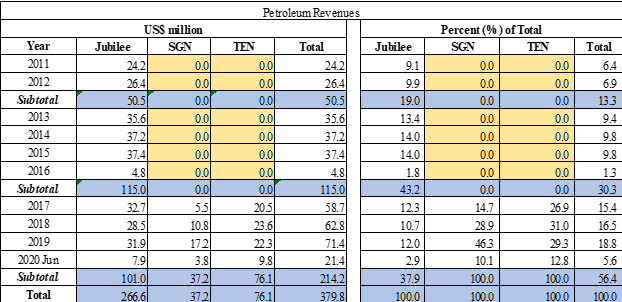

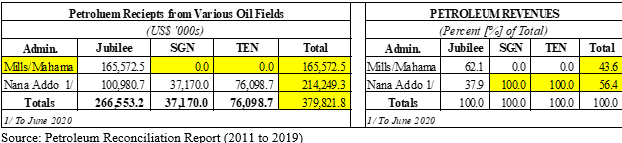

Table 1 shows the revenues from the Jubilee, TEN and Sankofa petroleum fields to the budget, including allocations to the statutory or sovereign wealth funds (SWFS) under the Petroleum Revenue Management Act (PRMA).

Table 1: Revenues from Petroleum Fields

- Nana Addo is lone beneficiary (100%) of Sankofa/TEN since 2017

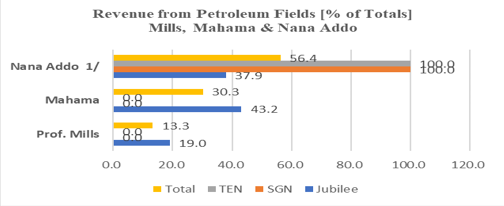

In addition to Jubilee from 2011, the current government inherited the entire output and revenues from Sankofa/TEN—with Mills/Mahama investments in all 3 fields while Nana Addo continues to reap the benefits. Table 2/Figures 1/2 show two 100% Sankofa/TEN bars for Nana Addo and zero (0%) for Mills and Mahama.

From the total of US$380 million since 2011, Nana Addo got US$214.2m (56.4%) in three-and-half (3.5) years compared to US$50.5m (13.3%) in one-and-half (1.5) years for Mills and Ghc115m (30.3%) for Mahama in (4) years. A total of US$113.3m from Sankofa (US$37.2m) and TEN (US$ 76.1m) went to only Nana Addo, with more flows expected to end-2020 to cement the unacknowledged gratuity.

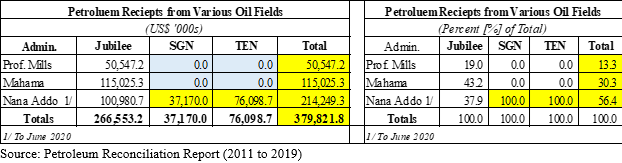

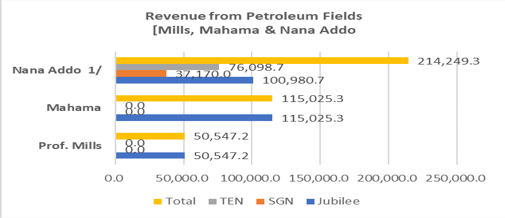

Table 2: Share of petroleum revenues from 2011

Figure 1: Petroleum revenues from oil fields (US$ ‘000)

Figure 2: Petroleum revenues from oil fields (% of Totals)

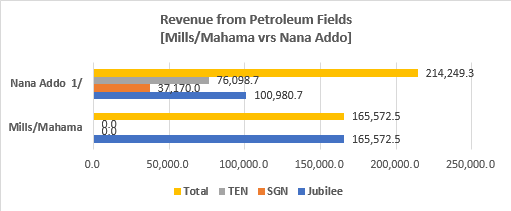

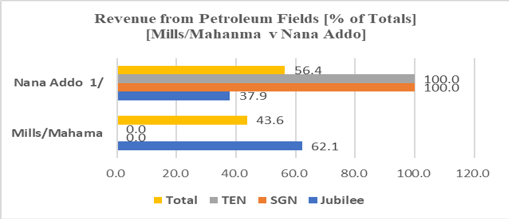

- More flows for Nana (3.5 years) than combined Mills/Mahama (6 years)

Table 3/Figures 3/4 show revenues to economy rising rapidly under Nana Addo in 3.5 years (US$ 214.2m or 56.4%) than the combined flows for Mills/Mahama (US$ 165.6m or 43.6%) in 6 years. Even with Jubilee (2011), Nana Addo has earned 37.9 percent of the revenue against 62.1 percent for Mills/Mahama combined.

Table 3: Combined Mills/Mahama versus Nana Addo flows

Figure 3: Combined Mills/Mahama versus Nana Addo flows

Figure 4: Combined Mills/Mahama versus Nana Addo flows

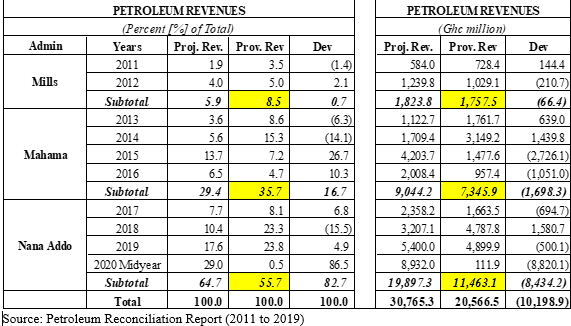

- Nana Addo has highest pre-COVID-19 SWF/Budget flows

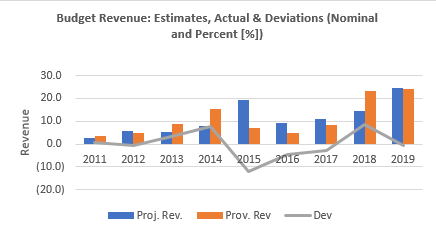

The PRMA allocates all oil/gas revenues to the Budget (ABFA), Stabilization, and Heritage Funds—after approval of GNPC’s share by Parliament. Table 4/Figure 5 show the estimates, actuals, and deviations for HE Mills, Mahama, and Nana Addo, with Mahama suffering the worst decline under the PRMA’s compulsory estimation rules.

The causes of the sharp decline are sharp crude oil price falls and damage to the Jubilee FPSO turret bearing. While they reduced crude and gas output from late-2014 to 2016, fortuitously, the price and output recoveries started from 2017.

Table 4: Petroleum revenue flows to the Budget

Figure 5: Graph of Petroleum Revenue Flows

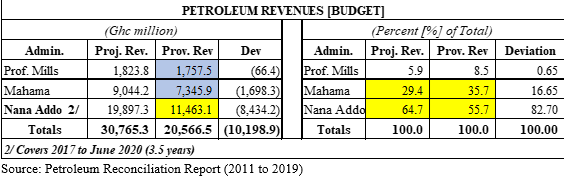

Table 5 shows that Provisional Actual revenues for Nana Addo in 3 years of Ghc 11.5b (55.7%) is higher than Prof Mills (Ghc1.75b or 8.5%) in 1. 5 years and Mahama (Ghc7.3b or 35.7%) in 4 years.

Table 5: Flows to Budget (Ghc and Percent {%} of Totals)

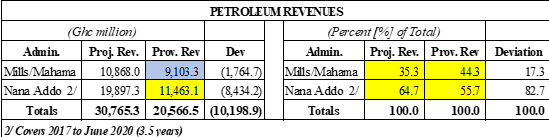

Again, Table 6 shows that Nana Addo’s Budget share of Ghc11.5b or 55.7% exceeds the combined Mills/Mahama share of Ghc9.1b or 44.3%—despite a potentially high deviation of 82.7 percent.

Table 6: Flows to Budget (Ghc and Percent {%} of Totals)

Conclusion

It is obvious from these data and explanation that the claims of inheriting a poor economy from the perspective of oil revenues is false. The distortion is to keep the lid on the consequences of an ambitious “consumption-based” economic agenda that is no longer convincing, politically.

As noted later, it hides the effects of false fiscal accounting that shows an exaggerated pace of fiscal consolidation is contrary to a faster pace of accumulating public debt. Unfortunately, the burst of compensating investment project is worsening the consequences of high pre-Covid-19 deficit and public debt misrepresentations, with harsh consequences for the entire economy.

Latest Stories

-

I’ve no plans to leave comedy for movie production, says Basketmouth

39 mins -

Akufo-Addo seeks to use Bawumia to complete Akyem Agenda– Asiedu Nketiah

47 mins -

‘Bawku conflict politicised for electoral gains’ -Martin Amidu alleges

49 mins -

‘Let industry players play the game ‘ – AOMC boss slams political interference in oil sector

2 hours -

Let’s learn from ExxonMobil, high flyers must lead the way for mergers – AOMC Boss

2 hours -

‘So many regulations, yet corruption prevails’ – Dr Riverson Oppong on OMC oversaturation

2 hours -

At least 24 dead after two boats capsize off coast of Madagascar

3 hours -

Madina MP lauds White Chapel Youth Group for championing peace ahead of elections

3 hours -

Man United settle for draw at Ipswich Town in Amorim’s first game in charge

4 hours -

GPL 2024/2025: Prince Owusu screamer earns Medeama win over Young Apsotles

4 hours -

BBC visits mpox clinic as WHO says DR Congo cases ‘plateauing’

4 hours -

Burning old TVs to survive in Ghana: The toxic trade in e-waste

4 hours -

Perfume boss admitted he ignored Russia sanctions

4 hours -

Wicked proves popular as opening set to be biggest for Broadway film

4 hours -

Nominee for agriculture secretary completes Trump cabinet

4 hours